This China Executive Briefing examines China’s post-COVID economic outlook focusing on the ‘dual circulation’ strategy and its expected impact across the Belt and Road Initiative, domestic markets, tech regulation and heavy industry.

Introduction

The outlook for H2 growth in the PRC is bleak. While not in a nosedive, the economy is preparing for greater risk. Reflecting post-COVID, post-Trump realities, Beijing is tacitly pursuing a least-worst strategy in macro-economic and trade policy. Tech innovation and smarter industries will propel an ultra-large domestic market; high consumption will realise national self-sufficiency. But, counter to Xi’s wishes, reliance on exports is still growing.

Video: China’s dual circulation strategy

Date: Tuesday 14th Septermber 2021 – 10am AEST

Speakers: Philipp Invanov – CEO Asia Society Australia | Bates Gill – Head of Department, Professor of Asia-Pacific Security Studies, Macquarie University | Sara Hsu – Visiting Scholar, Fudan University | Freda Zhang – Consultant APCO

Beijing is facing a slowing economy, a trade war with little hope of resolution and a global pandemic. Transition to slower growth has been dubbed the ‘new normal’ for the best part of a decade. But, as Beijing tries to secure its grip on power and prepare for demographic change and carbon neutrality, more aggressive attempts to shift the economy are on the way.

At the same time, ‘common prosperity’—a better sharing of the pie—sees a retreat from PRC-style neoliberalism (growing the economy while downplaying welfare). Per capita GDP is no longer the only yardstick; fairer access to public goods and better living standards are now central measures of economic success.

‘Dual circulation’ integrates these goals with the political imperative of self sufficiency. Emerging as a dominant paradigm, it reconciles slower growth with China’s fears of decoupling from global markets.

chart 1: China’s long term slowdown

source: World Bank

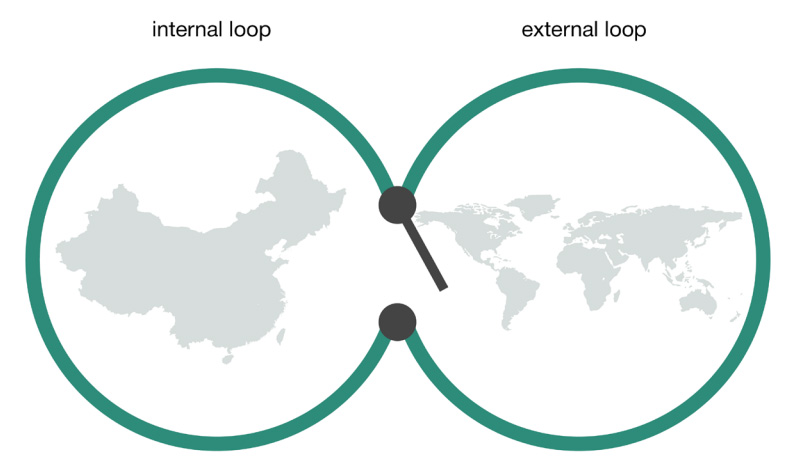

Dual circulation

Intended to foster autarky (see CEB Feb 2021 ‘open to autarky’), the concept envisions two loops, an inner domestic and outer global. The inner loop, ‘domestic circulation’, assumes growing consumer spending will spur domestic competition and innovation, creating quality products from a smarter industrial sector, well-paid jobs and disposable income to buy more PRC-made goods.

The outer loop, ‘external circulation’, is the global economy. International trade is still welcome, but the domestic loop is to become primary, insulating the PRC from external shock. Tech dependence on the US and others will cease to be an issue. A year after it gained central backing, dual circulation has become the macro-policy centre piece.

Global engagement: new best friends

Despite the rhetoric of reducing external exposure, international trade still powers the economy, entrenching its value. COVID-19 and commodity price hikes confirm PRC reliance on imports of global commodities and tech hardware; surging exports through H1 generated the bulk of growth. Official data show exports growing at some 32 percent y-o-y, propelling the recovery, as import growth slowed to some 37 percent. Exports are projected to slow y-o-y in H2 due to shipping chaos, surging COVID variants and a cooling geopolitical climate.

chart 2: exports are still growing

note: Jan figures reported with Feb, causing spikes in 2020 and 2021.

source: State Administration of Foreign Exchange

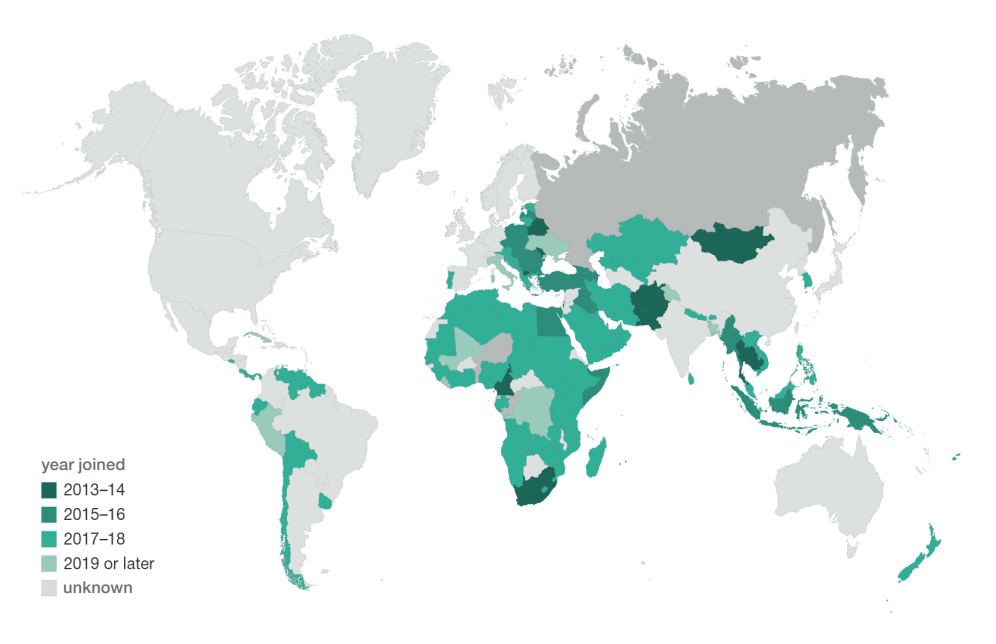

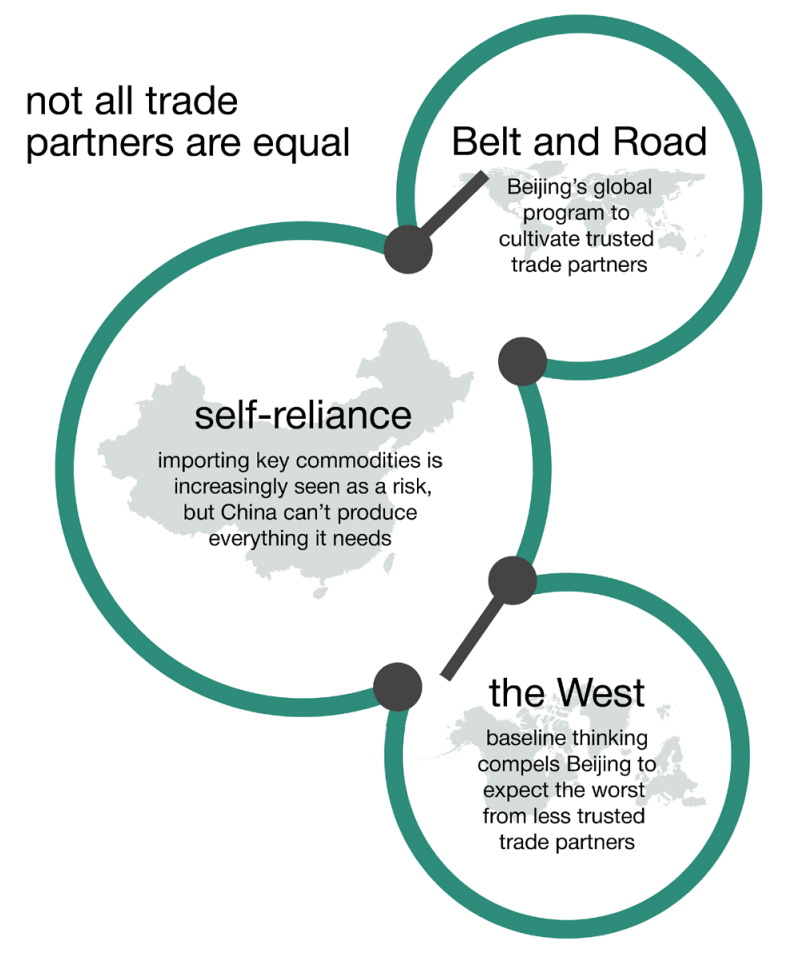

Sourcing commodities along the Belt and Road

A blend of self-reliance, overseas investment and diversification make up the BRI (Belt and Road Initiative), Beijing’s favoured global engagement policy. A quasi Marshall Plan underpinning PRC-style globalisation, it is evermore embedded in economic policy. Expanding China’s trade reach, the BRI is moving beyond conventional infrastructure to high-tech, green development; the digital economy; and industrial and agricultural development. Overseas production controlled by PRC entities is deemed part of the internal loop of dual circulation. In the long term, this should worry China’s trade partners.

map 1: the BRI extends across the globe

source: Belt and Road Portal, State Information Centre

Diversifying import sources

Iron ore is a prime example of Beijing’s aspiration to control overseas production. Over 1 billion tonnes were imported in 2020 (80 percent of total supply); Australia was the source of some 60 percent. A draft measure mooted in January 2021 called for 45 percent of domestic demand to be met by local sources (iron ore, scrap steel and pig iron) by 2025, up from 37 percent in 2020. The draft foresees a 25 percent increase in scrap steel use, to 320 million tonnes per year, the equivalent of some 500 million tonnes of medium grade iron ore. In addition, 20 percent of imported ore is to come from PRC-owned mines abroad.

Bids to locate more diverse iron ore supply options come as no surprise. Cooperation with neighbours Russia, Myanmar, Kazakhstan and Mongolia is highlighted, in tandem with developing sources in Southeast Asia, central Asia and Africa.

International firms subject to global tensions may lose out either way. Those that provide needed tech will be welcomed by the PRC, but their home countries may not be so enthusiastic. In addition Beijing is bolstering its legal toolkit to counteract long-arm laws of other countries, but how and when new measures will be used remains unclear. Rising domestic competition and increasing regulatory oversight will also complicate the outlook for global players.

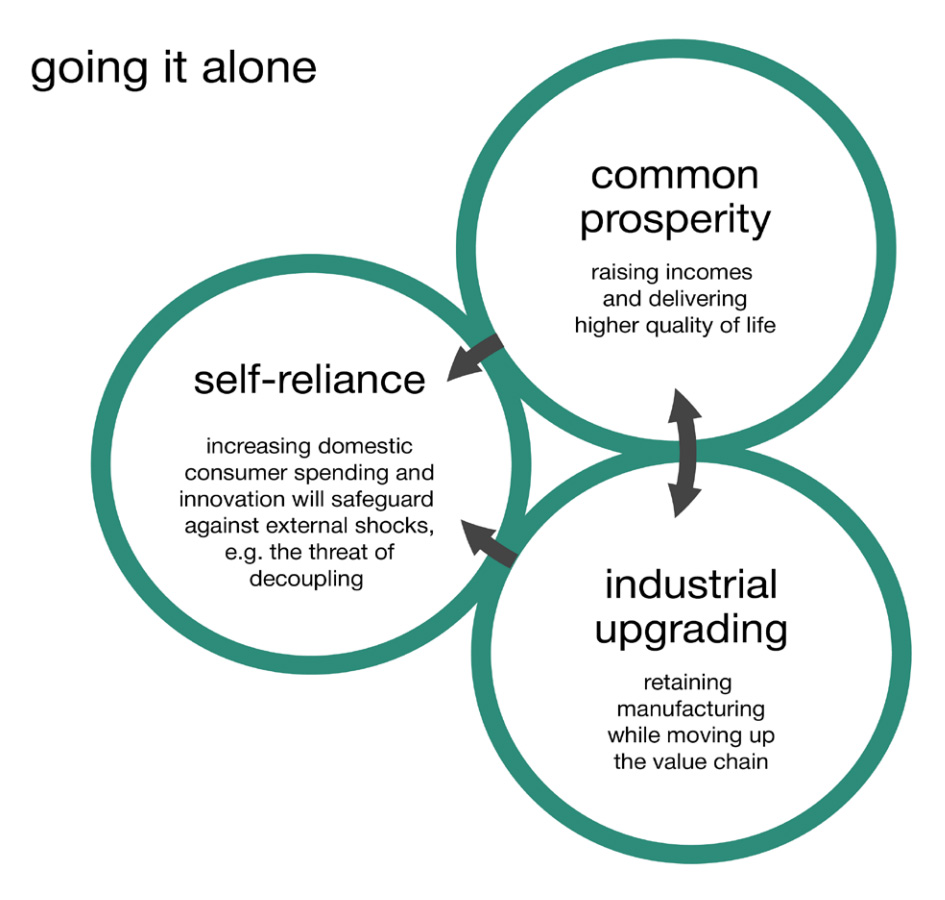

Creating an ultra-large domestic market

Vaunted as becoming ‘ultra-large’, the domestic market (plus its enclaves in BRI countries) aims to fuel virtuous cycles of consumption and innovation in pursuit of self-reliance.

Consumer spending

Vital to dual circulation, consumption has slowed as spenders hedge uncertainty over their future incomes. This is a concern: under dual circulation rising consumption was intended to balance slowdown in exports. Beijing is seeking to engineer more spending primarily by addressing housing affordability. Developers are rewarded for building cheaper rentals, while purchasing loopholes are being closed to reduce property speculation.

Slowing growth

Exports and real estate investment were obstinately strong in Q2, yet consumer spending and other drivers remained weak. Economic growth in Q2 2021 slowed to 7.9 percent y-o-y from a COVID-induced low base; local pundits had forecast 8.2. Supply and demand have continued to diverge; SMEs are struggling.

Softening the landing

Debt controls were eased in 2020, allowing some stimulus to be directed at SMEs and avoiding overspending on fixed assets with low returns. In a 30 July meeting, the Politburo indicated fiscal spending will continue to be the tool of choice to counter a slowdown, expected to continue until year end.

Some controls are still in place. Brakes were applied to project approvals by the planning ministry, and funds performance monitoring suggested by the finance ministry. To date, fewer special purpose bonds (issued by localities to fund infrastructure projects) have been floated in 2021 than in previous years.

Ever fearful of hard landings, localities are proffering tax and fee cuts. But SME profits are still squeezed by anaemic market demand and rising commodity prices. Nationally, the central bank (PBoC, People’s Bank of China) cut the required reserve ratio by half a percentage point in July, giving banks more money to lend. No change in monetary policy, PBoC insists—just a one-off adjustment.

Taming commodity prices

A minor easing of the reserve ratio for banks follows measures to curb price hikes in iron and steel among key commodities, in tandem with sales of strategic reserves of zinc, copper and aluminium. This is hoped to set de-facto price ceilings, easing pressure on downstream SMEs.

Commodity price hikes, assures PBoC, will cease in Q4 2021 and Q1 2022 as supply and demand settle. Assuming these price ceilings hold while prices hover near, PBoC will ease monetary policy in the short term, giving firms a chance to ride out high prices until the global economy normalises.

Bolstering R&D to decouple finance

A core aspect of decoupling is in finance. Yet Beijing is looking not to decouple, but to refocus international engagement. Shanghai will be key: a measure on opening in the Pudong New Area puts this into practice. Financial opening will be conditional on attracting ‘hard-tech’. Industries like integrated circuits, life sciences and AI are called on to intensify their R&D. Improving foreign debt management and easing restrictions on foreign engagement in the STAR Board (Shanghai’s Nasdaq) will follow.

Disciplining the private sector

Beijing wants control back in its own hands. Data (and their controlling algorithms) are now the key economic input, the gold of the ‘new development era’. Tech giants—seen as willfully challenging economic stability, stifling competition, hoarding their gold and widening inequity—are public enemy number one. But they are not alone: reining in other sectors that go against Beijing’s wishes to now split the pie more evenly will be the norm.

Crackdown on tech giants

Hence the gunfight at the data corral. Alibaba, China’s tech behemoth, was fined a record C¥18.2 bn in April 2021. The ‘exclusive deals’ (forbidding merchants to use multiple platforms) it imposed on merchants were torn up by the regulator, setting a marker for the platform economy. Didi, China’s ride-hailing colossus, was raked over the coals largely for the vast scale of its data hoard. Meituan and other IT-driven dispatchers face the same fate over the labour rights of riders, employed on precarious contracts and poorly paid.

Break-up, the likely fate of similar giants in the EU or US, is not on the cards. Smaller firms may be funded to build out their position in virtue of critical niche roles in industrial chains; yet Beijing is, in most sectors, consolidating ‘national teams’ of a handful of firms.

The United Front Work Department (an arm of the CCP that keeps a hand in non-Party affairs) is making the Party ever more present in private tech firms and SOEs are investing in them, a further tentacle of state control. This new economic model is blending a top-down, visible hand with market efficiency. Necessary to provide tech solutions while domestic industry catches up, innovative international players are expected to play by the same rules and help meet national goals. This is doubly so for international investors.

Less visible globally but no less newsworthy than Alibaba founder Jack Ma, Zhang was in 2018 accused of publishing unsavoury content on Bytedance apps, and in 2020 for kowtowing to the US when planning to sell TikTok to Microsoft/Oracle. Prior to his fall from grace, Zhang, like Mark Zuckerburg, deemed tech intrinsically positive and needing no oversight (a view not shared by the CCP). Zhang is nonetheless fiercely independent: Bytedance remains the sole PRC internet major not hanging on Alibaba or Tencent purse strings. Zhang announced in May 2021 that he will step down by year’s end.

Zhang Yiming 张一鸣

Bytedance founder

Less growth, better growth

Ideally, growth will come mostly from productivity gains, which must grow ever faster to offset the coming decline in the working population. Looking after the ageing aligns with ‘common prosperity’ goals in that it shifts the focus from GDP growth to concentrate instead on quality of life issues. This in turn chimes with the rising importance of environmental and climate goals. The production loss implied by the CCP’s carbon goals—peaking by 2030, neutrality by 2060—is to be mitigated by innovative, greener tech (see our next CEB issue).

Beijing is betting on high-end manufacturing and consumer spending to herald a ‘new development era’. Common prosperity brings into sharp relief the downside of the CCP’s long preference for growth over equity. The state now seeks to break the dominance of private capital across economic sectors and retake control of the economic levers as part of its march to autarky.

Get the latest briefings as soon as they go live with our newsletter!